Financial document translation: terminology, glossary, and workflow tips

Financial translation requires precise terminology and a structured workflow. Here's how to build a glossary and deliver error-free financial documents.

Financial translation sits in a category where a mistranslated term or a misformatted number can create real legal and regulatory exposure. We've worked with agencies handling financial document translation across multiple language pairs, and the same pattern shows up: projects that go smoothly are built on solid preparation — a real glossary, a clear sense of what type of document you're working with, and a QA process that accounts for finance-specific risks. The projects that don't go smoothly are usually missing one of those three things.

What makes financial translation different from other business documents

Financial documents carry specific structural expectations. An annual report, a bond prospectus, or an audit opinion isn't just formal business writing; it's a genre with its own conventions, regulatory framing, and required terminology. Readers on the target side (auditors, regulators, institutional investors) will notice immediately if a term diverges from what's expected in their market.

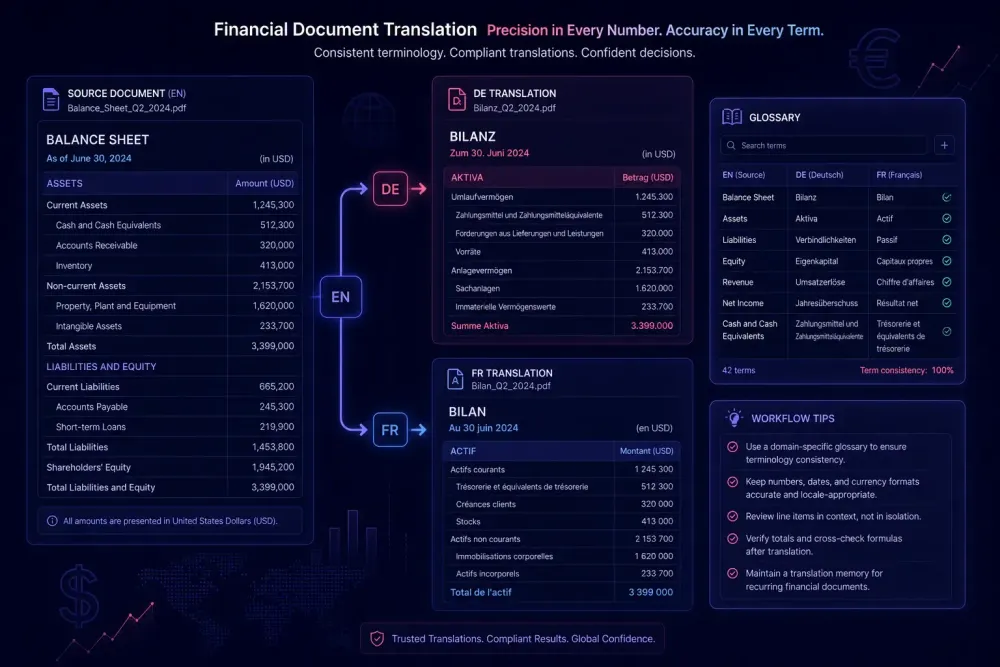

Regulatory terminology in finance is largely fixed. Terms like "consolidated statement of financial position," "fair value through profit or loss," "other comprehensive income," or "going concern" are not paraphrases. Under IFRS, US GAAP, or applicable national accounting standards, these expressions correspond to defined concepts. Translating them freely, even when the result reads naturally, creates ambiguity or outright errors in audit-ready deliverables. We've seen cases where a well-intentioned attempt at a more fluent local equivalent produced a document that confused the client's external auditor during review.

Numbers and formats carry meaning too, and this is where financial translation diverges most sharply from general document work. Decimal separators, thousands separators, and date formats differ across locales. Translate a document from English to German and leave commas and periods as-is, and you get a document that reads grammatically but presents numbers incorrectly. The figure 1,234.56 in English becomes 1.234,56 in German convention — without a dedicated numbers check, this slips through standard linguistic QA entirely.

The third difference is audience. Financial readers — CFOs, external auditors, compliance officers — aren't reading for general comprehension; they're verifying whether the translated document reflects the same financial position as the source. That changes the review standard from "does it read well" to "does it mean the same thing precisely." These aren't the same question.

This doesn't mean financial translation requires an accounting qualification. But it does require translators who have worked with the specific document types and have access to current, approved glossaries for the applicable accounting standard. Domain exposure matters more than general business language competence.

Building a financial glossary before the project starts

One of the most consistent patterns in financial translation projects that run into trouble is the absence of a glossary at intake. A translator picks a term in the first document, it propagates through fifty pages and multiple associated files, and by the time someone catches the inconsistency the revision scope is significant.

A practical financial glossary for a recurring client should cover primary financial statement line items (assets, liabilities, equity, revenue, operating profit), standard accounting terms from the applicable framework (IFRS, US GAAP, or local standard), entity-specific terms (subsidiary names, trademarked product categories, internal department labels), and regulatory references (names of regulations, supervisory bodies, and relevant filings).

For agencies working with financial institutions, a second layer often matters: securities terminology (bond, coupon, maturity, tranche, warrant, repo), and for clients who operate derivatives, a short list of instrument names and their approved translations. This isn't exotic — most banks and asset managers have existing approved glossaries in at least one language pair. The first question at intake should be: "Do you have previously translated documents we can mine for term pairs?"

The glossary doesn't need to be exhaustive to be useful. A targeted list of 80–120 terms assembled before work starts outperforms a comprehensive termbase that no one updates. A reliable starting point for IFRS terminology is the IFRS Foundation's published translations of IAS/IFRS standards, which provide official parallel-text term pairs in over 50 languages. These are public and free — most agencies working on IFRS financial statements should have them accessible.

One rule we follow consistently: financial glossary terms go through client sign-off before work starts. The client's finance team, not the translation team, should confirm how they want "adjusted EBITDA" or "non-controlling interests" rendered in the target language. That approval step eliminates one of the most expensive revision categories: the client who sees a correctly translated but internally inconsistent term at delivery and asks you to change it throughout.

For a broader framework on building and maintaining terminology assets, our guide to translation terminology management covers the full workflow.

Financial document types and why they require different approaches

Not all financial documents are the same, and treating them identically is a reliable source of problems. A loan agreement and an annual report may have similar word counts, but they're different translation engagements with different risk profiles.

Annual reports and quarterly filings typically mix narrative sections (chairman's letter, business overview, risk disclosures) with tabular financial statements. The narrative sections have more translational flexibility; the statement pages don't. In practice this means different handling within the same file: narrative sections can go through standard translation and post-editing, while statement pages benefit from a strict TM approach where confirmed term pairs are locked and not subject to fuzzy-match substitution. Applying the same fuzzy-match logic across both sections introduces unnecessary risk.

Prospectuses and offering memoranda are long, repetitive, and legally significant. These documents are written to be read by regulators, and translation errors can create compliance exposure. The repetition makes them strong candidates for translation memory, but the sensitivity means fuzzy-match logic needs human review before confirmation, not automatic acceptance. A match at 85% may look safe but carry an incorrect number inside the segment.

Audit opinions and management letters are short, formulaic, and almost entirely fixed-phrase. A standard Big Four audit opinion in most markets has an established template. The right approach is near-verbatim translation following the firm's standard language, not creative paraphrase, regardless of how natural the alternative might sound. These documents have established conventions precisely because the words carry specific professional and legal weight.

Loan agreements and credit facilities overlap financial and legal translation. They combine accounting definitions, calculation mechanics (margin structures, SOFR-based rate references, financial covenants), and contract law clauses. Both financial and legal terminology coverage need to be confirmed in the project scope — this is not a document type to hand to a specialist in only one of the two domains.

Numbers, tables, and format consistency

Format inconsistency in financial documents is the most common QA failure we encounter, and one of the hardest to catch in a standard linguistic review. A QA pass built for prose catches grammar and terminology; it misses a misplaced decimal separator in a financial table.

The format check needs to cover specific areas. Decimal and thousands separators: confirm the target locale convention and check every number in the document. In French and German, the decimal separator is a comma; in English it's a period. A single incorrect separator changes the meaning of a figure numerically, not just visually. Date formats: DD/MM/YYYY vs. MM/DD/YYYY creates real ambiguity for any date written as 01/04/2025. Regulatory filings often use spelled-out month names for exactly this reason. Currency symbols and codes: whether to use €, $, £ or EUR, USD, GBP is a client convention, but it needs to be consistent throughout the document and aligned with target market expectations.

Table alignment is the one that tends to get scoped out and then causes problems at delivery. Translated text in financial tables often expands or contracts relative to the source — a row label that fits one line in English may run to two in German or collapse in Japanese. This creates formatting breaks that require a DTP review pass before delivery. If DTP review isn't in scope, flag it to the client at the outset so there are no surprises.

Running a find-and-replace search for numeric patterns as part of the QA workflow catches the obvious cases. Tools like Xbench or Verifika have configurable number-check rules that can automate part of this pass, though they require correct locale settings to work — a tool configured for English-locale checking will not flag a German-convention number error.

Translation memory strategy for financial projects

Financial documents reward a structured TM approach more than almost any other document type. Financial reporting language is highly repetitive within and across documents: the same boilerplate — risk disclosures, accounting policy notes, segment definitions — recurs every quarter with minor updates. A TM built over two or three reporting cycles can pre-translate 40–60% of a quarterly report before any new work begins.

The catch is TM quality. If a client's TM was built on rough drafts or contains uncorrected errors, those errors propagate into every subsequent document. Before relying on a client's existing TM for a financial project, run a quality audit on the highest-frequency segments. A handful of bad entries in the accounting policy notes section will appear in every quarterly filing.

For new financial clients with no existing TM, the fastest path is to request two or three previously translated documents, import them as parallel files, and build a reference TM from confirmed segments. Even a small TM of 500 to 1,000 segments pays off on the first live project.

One approach that works well on recurring mandates: assign consistent translators to consistent document sections across multiple projects. The person who always works on the accounting policy notes section builds implicit domain knowledge and catches period-over-period changes that someone new would miss. It's not always feasible in agencies with high freelancer turnover, but where it's possible, the revision rate drops noticeably and the client notices.

This works best when the TM is client-specific, not just domain-specific. Financial reporting terminology for a European bank is not the same as for a US private equity fund. A generic "financial services" TM will give you consistency across the wrong terminology set.

QA for financial documents: what standard checks miss

Standard CAT tool QA — spelling, tag verification, terminology flags — covers the linguistic surface of a financial document. It doesn't cover domain-specific risks. A financial QA pass needs to add checks that general QA doesn't include.

Glossary compliance: every approved term in the source should appear in the target using the correct equivalent. This matters especially for IFRS line items, regulatory definitions, and entity-specific terms. If your CAT tool or QA tool supports glossary enforcement, configure it against the client's approved list, not just generic dictionaries. A generic financial dictionary gives you translations; an approved client glossary gives you the right ones.

Numerical consistency: every number in the source should appear in the target with the correct value, correct locale format, and correct position in context. Automated number checks catch missing or transposed figures, but they require correct locale configuration. A tool set to English-locale checking will not flag a German-convention number error.

Segment count integrity: financial documents sometimes see segments dropped during file processing, particularly in tables. We've had deliveries where a table looked visually intact but was missing a row because it was lost during file conversion, and the client's finance team caught it during their review. A segment count comparison between source and target at the file level should be part of the sign-off process, not something you discover after delivery.

Building a client-specific QA checklist that includes these domain checks alongside the standard linguistic review significantly reduces the revision rate on financial projects. Our post on translation quality assurance for agencies and freelancers covers the broader QA framework in detail.

Takeaway

Financial translation is a discipline where preparation determines the outcome. Before a project starts, confirm the applicable accounting standard and its approved target-language terminology, build a glossary from prior translations or official IFRS/GAAP parallel texts, and establish which document type you're dealing with — the risk profile for a quarterly report is different from a prospectus, which is different from an audit opinion. During delivery, a dedicated format QA pass checking number separators, date formats, and table structure catches errors that standard linguistic review misses. For recurring financial clients, investing in TM quality from the start compounds: the third quarterly filing with a well-maintained TM requires a fraction of the post-editing effort of the first.